Introduction

In our previous Salient Point (Issue 3), we discussed how a company could go about preparing a cash flow forecast. Such a forecast, as mentioned in that article, could be helpful to improve the company’s cash flow visibility under uncertain times. Additionally, a cash flow forecast could be used to determine the value of the business using the discounted cash flow (“DCF”) method. Such a valuation could be used for, amongst other things, fund-raising, impairment assessment and/or reporting to stakeholders.

To conduct a valuation using the DCF method, in addition to a cash flow forecast, a discount rate estimate is needed to present value the forecast cash flows. In this article, we discuss aspects of the discount rate that would be helpful to know if you are estimating or reviewing one.

Reviewing inputs to a discount rate estimation

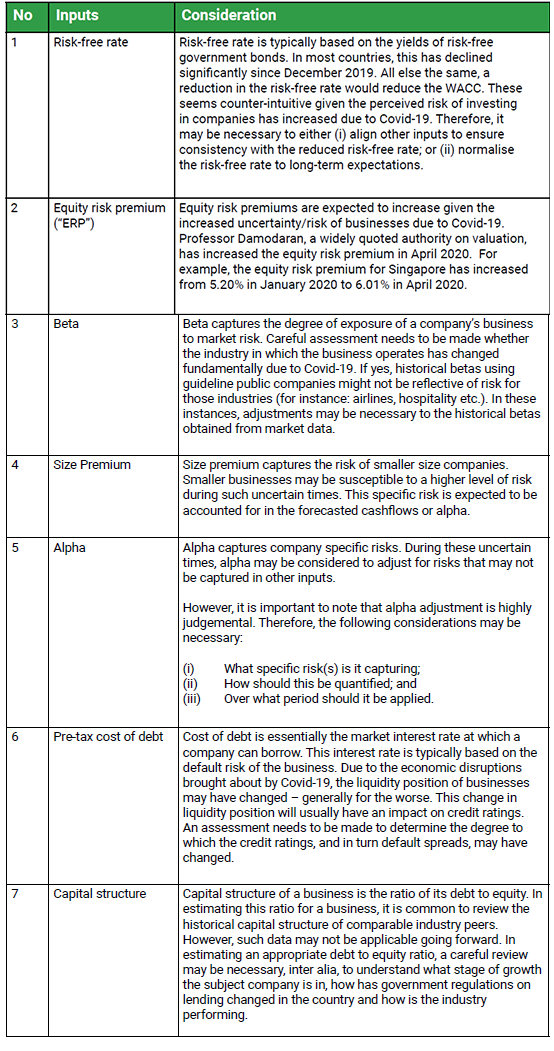

Typically, the discount rate used to present value forecast cash flows of a business is the weighted average cost of capital (“WACC”) of the business. There are various inputs that go into estimating a WACC for a business. Below, we discuss these inputs and their considerations under uncertain times.

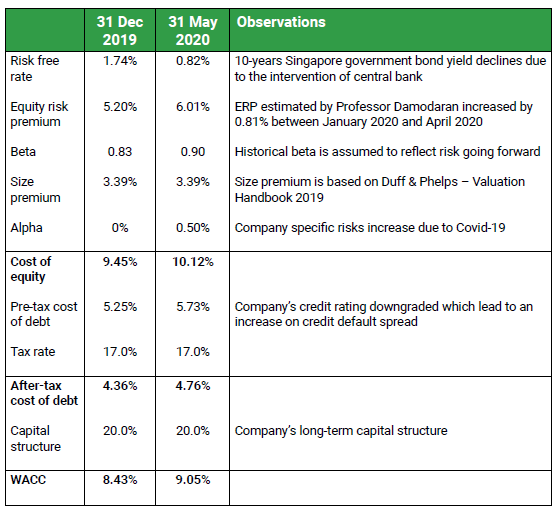

Based on the comments provided above, we have illustrated a WACC for a private company based in Singapore as at 31 Dec 2019 (Pre-COVID-19) and 31 May 2020 (Current) in the table below.

Careful consideration should be given in estimating the WACC of the business. The WACC is unlikely to be lower than pre-COVID-19, given that the level of risk in the investment is higher during these uncertain times.

Ensuring no double-counting of risk

Estimation of a discount rate cannot be done independently of the preparation of a cash flow forecast. If adjustments to cash flow forecasts have been made to take into account the effects of Covid-19 related disruptions, then adjustments to discount rate need not be as high as they would have been if no adjustments to cash flows were made. This approach ensures that the risks to the business due to COVID-19 are not double-counted in both the cash flows and discount rate.

Using cross-checks may be imperative.

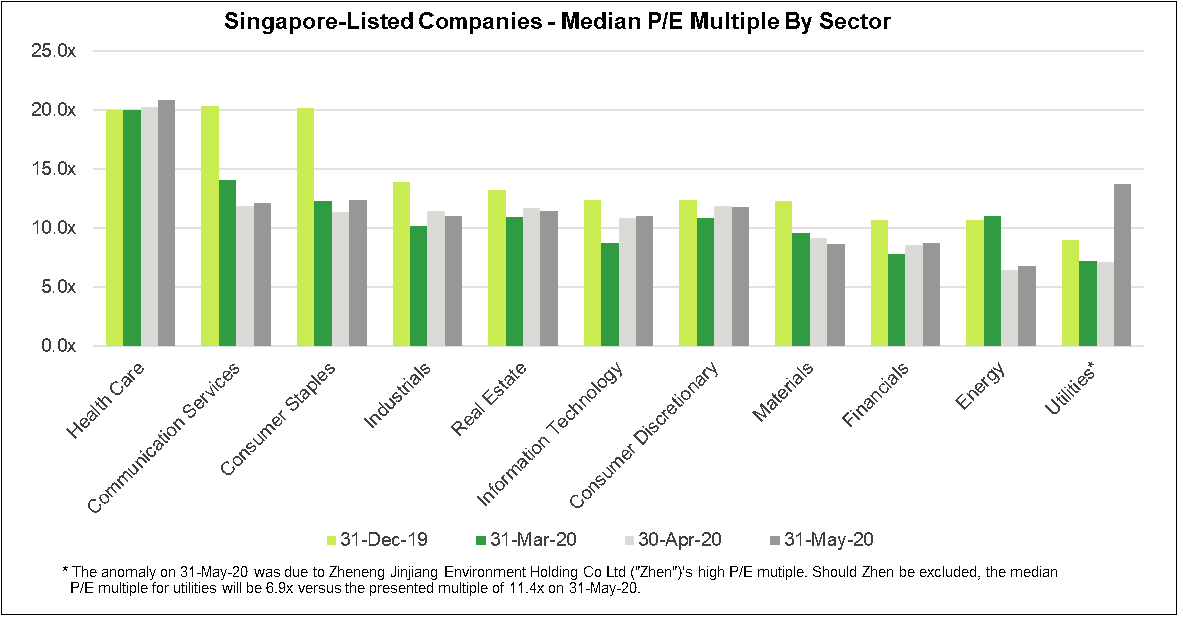

It may be necessary to cross-check the valuation outcome from the DCF method, given the uncertainties associated with preparing the cash flow forecasts and the inputs to the discount rate. We could compare the implied earnings multiple of the subject company against industry peers. Here, too, not all industry multiples have changed equally due to COVID-19.

It is important to note that such cross-checks have limitations. There may be company specific factors that may make comparisons to guideline public companies difficult. However, in general, such cross-checks will help build confidence in the valuation done using the DCF method.

How Baker Tilly Can Help

If you are looking to engage a valuer for your business needs during these uncertain times, our Deal Advisory department may be able to help you.

DISCLAIMER: All opinions, conclusions, or recommendations in this article are reasonably held by Baker Tilly at the time of compilation but are subject to change without notice to you. Whilst every effort has been made to ensure the accuracy of the contents in this article, the information in this article is not designed to address any particular circumstance, individual or entity. Users should not act upon it without seeking professional advice relevant to the particular situation. We will not accept liability for any loss or damage suffered by any person directly or indirectly through reliance upon the information contained in this article.

Related content